2023. 12. 26. 00:21ㆍ투자/논문리뷰

요약

- BTC, ETH, LTC의 2015~2019년 데이터를 토대로 intraday, nextday momentum 측정

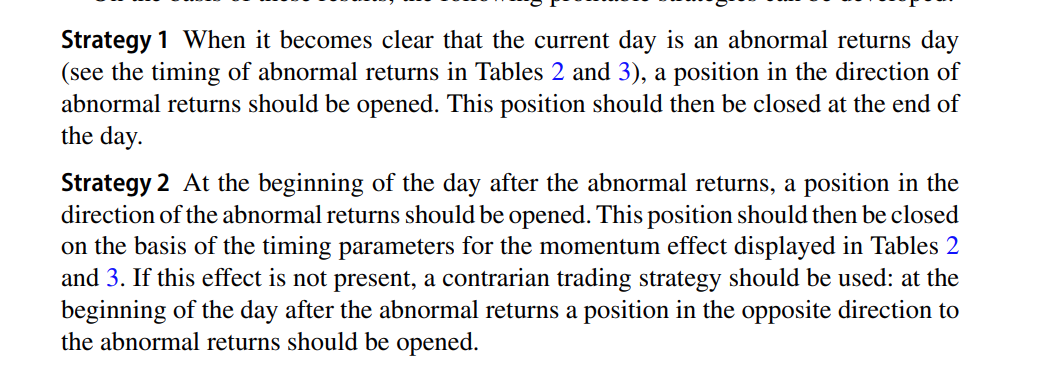

- 당일 특정 시간 이후에 abnormal한 날이라고 밝혀진 경우, 당일 끝까지 momentum이 존재.

- positive, negative 모두 해당됨.

Abstract

This paper examines whether there exists a momentum effect after one-day abnormal returns in the cryptocurrency market. For this purpose, a number of hypotheses of interest are tested for the Bitcoin, Ethereum and Litecoin exchange rates vis-à-vis the US dollar over the period 01.01.2015–01.09.2019, specifically whether or not: (H1) the intraday behavior of hourly returns is different on abnormal days compared to normal days; (H2) there is a momentum effect on days with abnormal returns, and (H3) after one-day abnormal returns. The methods used for the analysis include various statistical methods as well as a trading simulation approach. The results suggest that hourly returns during the day of positive/negative abnormal returns are significantly higher/lower than those during the average positive/negative day. The presence of abnormal returns can usually be detected before the day ends by estimating specific timing parameters. Prices tend to move in the direction of the abnormal returns till the end of the day when it occurs, which implies the existence of a momentum effect on that day giving rise to exploitable profit opportunities. This effect (together with profit opportunities) is also observed on the following day. In two cases (BTCUSD positive abnormal returns and ETHUSD negative abnormal returns), a contrarian effect is detected instead.

- Method

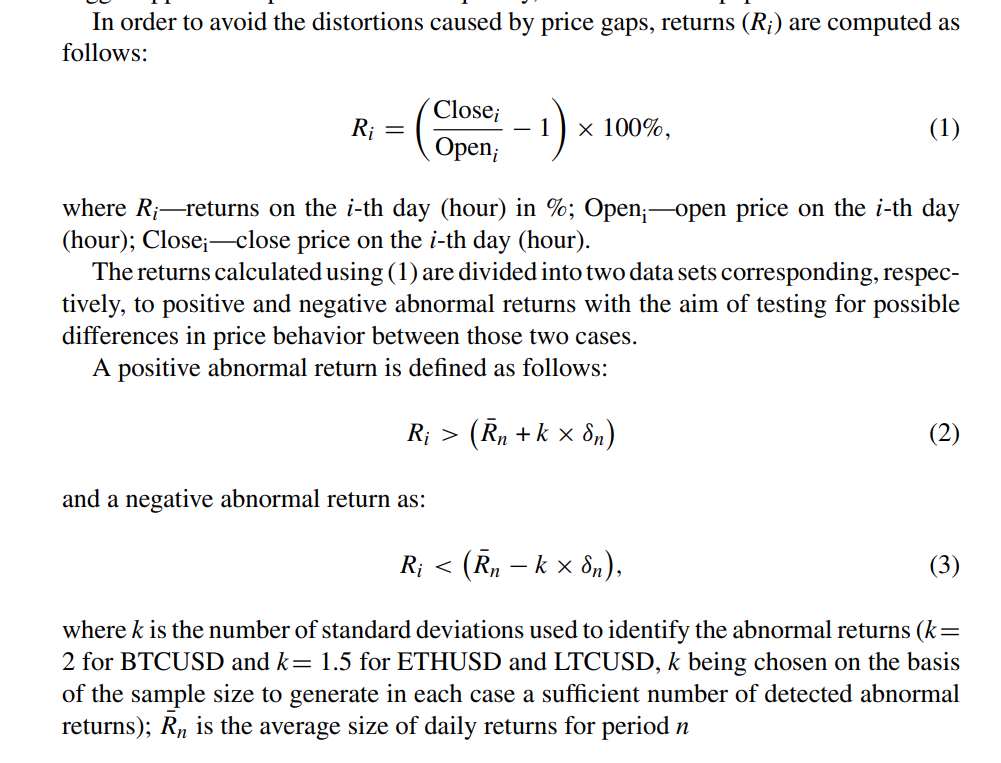

왜 BTC는 표준편차 2, 나머지는 1.5를 쓴걸까. BTC의 가격 움직임이 훨씬 안정적일텐데 표준편차도 더 큰 것을 사용한다? 뭔가 이상하다.

- Result

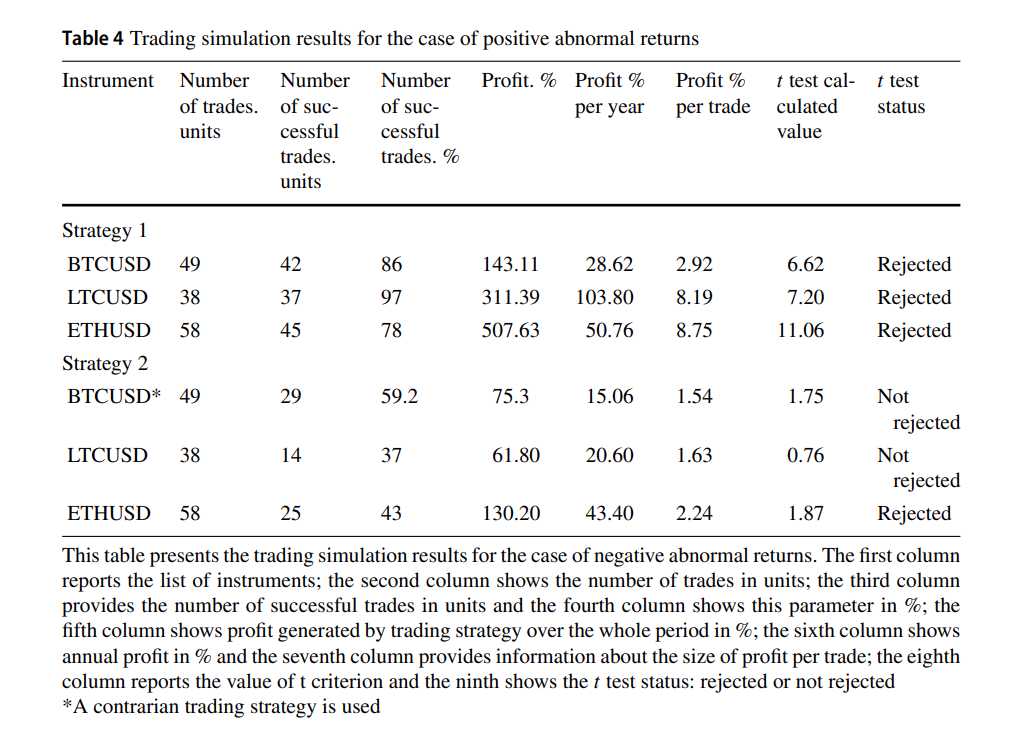

Positive, negetive 모두 intraday momentum 존재, nextday momentum은 2개만 존재하는 것을 알 수 있다.

intraday momentum의 t값이 압도적인데 비해 nextday momentum은 그닥이다. 내가 1ATR로 테스트했을 때는 승률 45% 정도에 average profit이 1% 정도였는데 비해 훨씬 좋다. 논문의 metric으로 다시 테스트를 해봐야겠다.

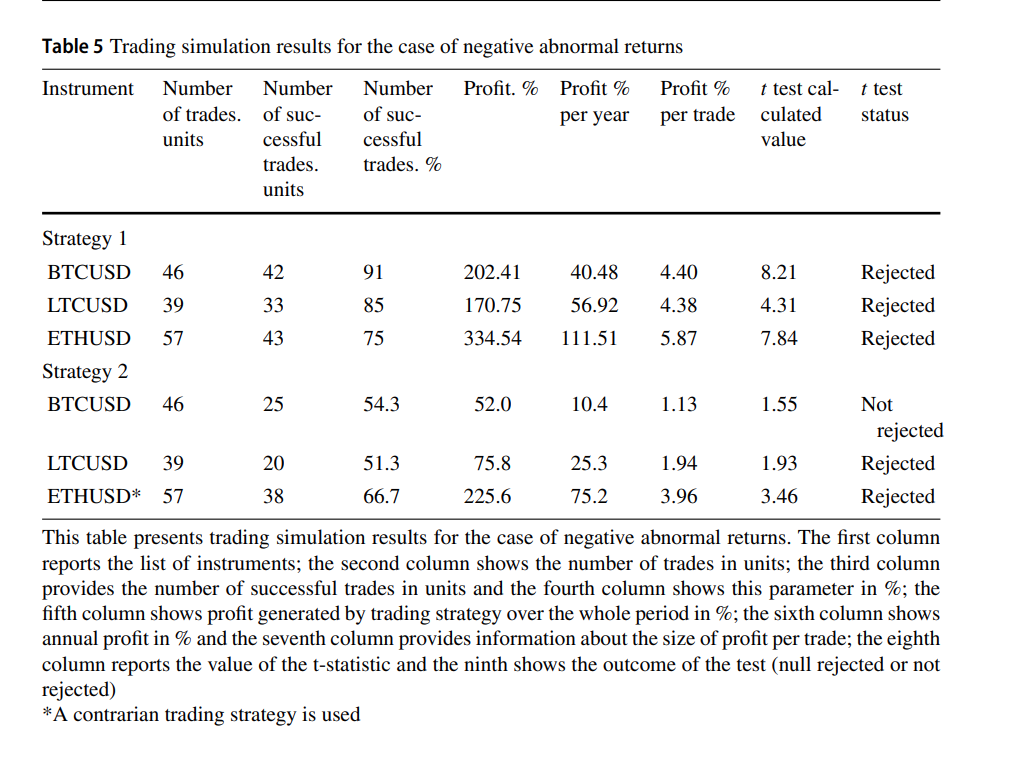

negetive로 했을 때도 마찬가지.

-구현 및 결과

논문에 평균 return을 며칠을 기준으로 구하는지 안나와있다... 일단 기본적인 20일로. k도 일괄 2로 적용.

당일의 특정 시간(12시, 14시, 16시...)가 되었을 때 시가로부터 현재가가 k표준편차 만큼 높다면 매수 후 24:00에 매도.

20200101-20230101 까지 binance futures로 max trade 100, fee 0.1%, stoploss 50% 조건

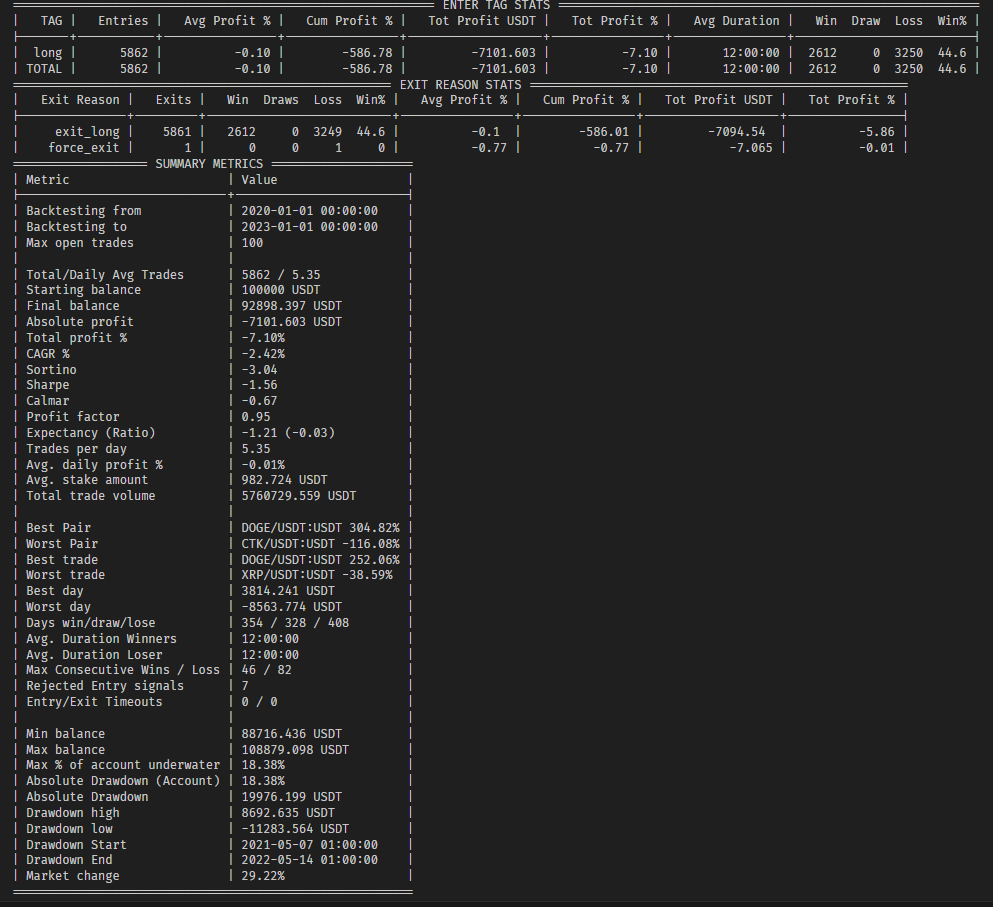

1-1. 12시 매수

안된다. ETH, BTC도 40%대 승률, BTC는 아예 손해다.

1-2. 15시 매수

흑자로 바뀌긴 했지만, 실망스럽다.

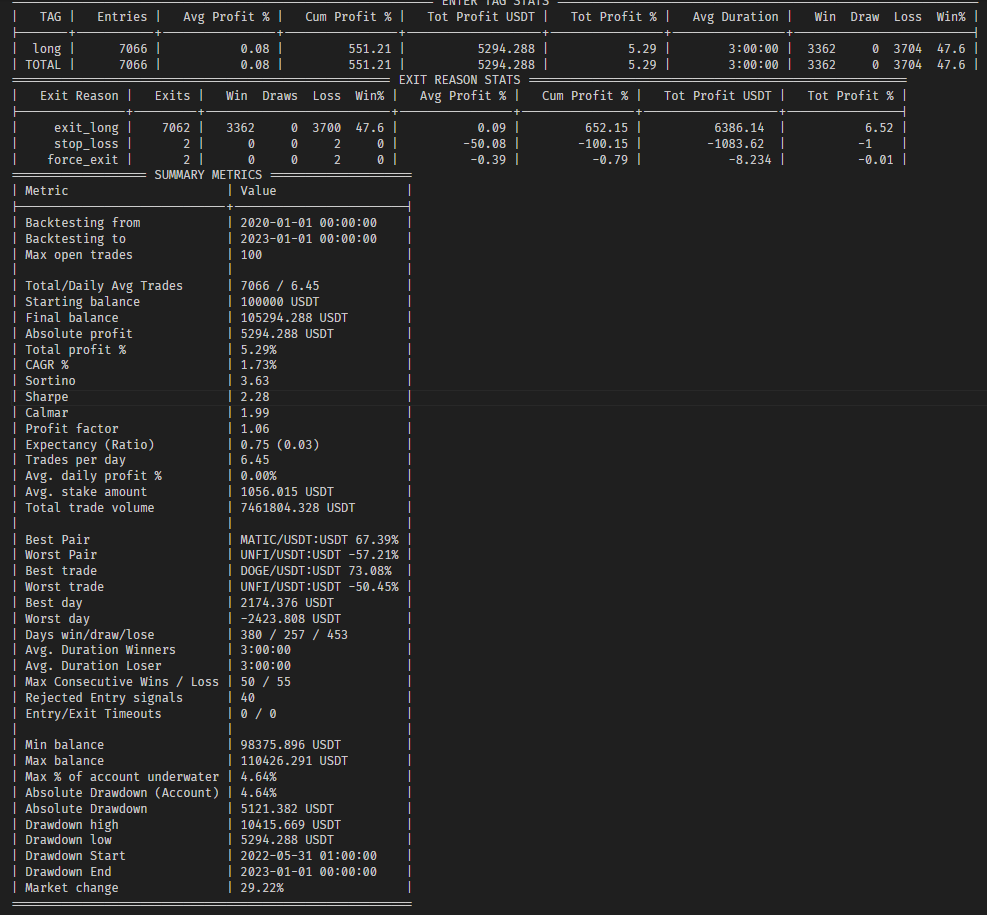

1-3. 18시 매수

확실히 보유시간이 짧아져서 샤프가 3.55에 mdd가 7.6이라는 환상적인 수치가 나왔다.

1-4. 21시 매수(?!)

역시 3시간은 모멘텀이 약하다. 그래도 아직 샤프가 2.28이니 short도 넣으면 더 좋아지지 않을까 싶다.

이번엔 short도 추가해서 실험해보자.

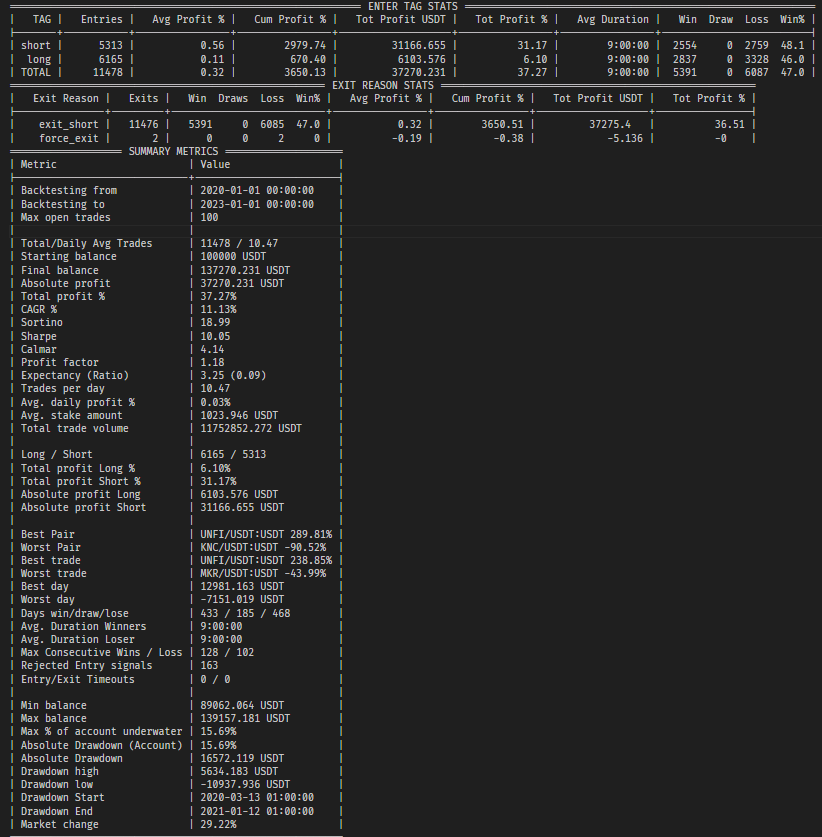

2-1. 12시 매수/매도

그만 알아보자...

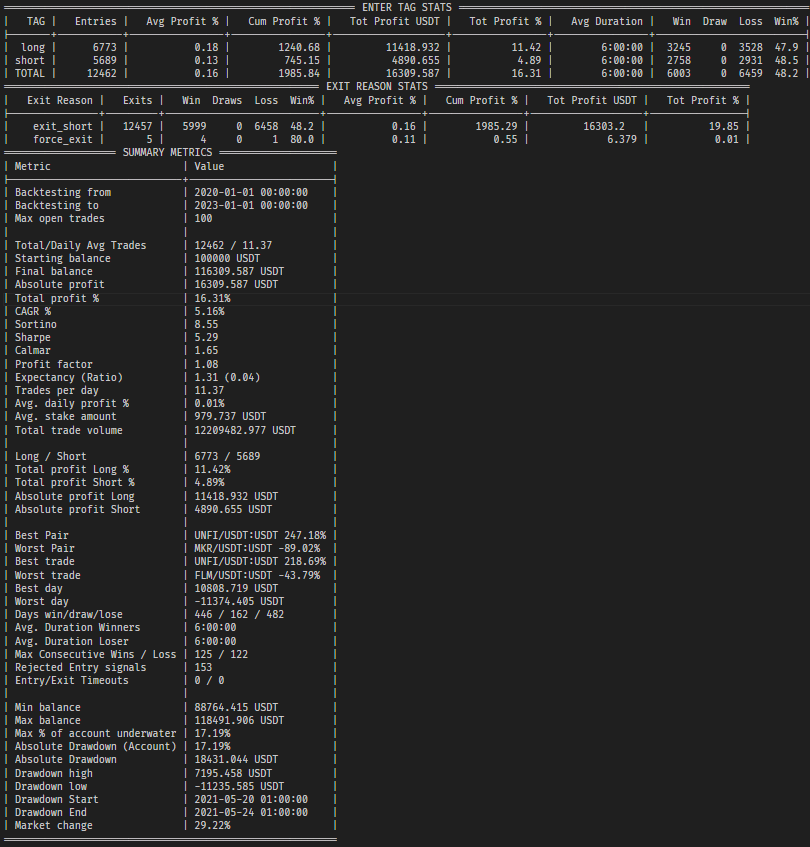

2-2.15시 매수/매도

short은 15시가 압도적으로 좋은데 왜일까... 게다가 샤프가 10???

2-3 18시 매수/매도

샤프는 5.29로 상승했지만, mdd와 Calmar도 상승했다.

2-4 21시 매수/매도

21시는 long only와 마찬가지로 별로이다.

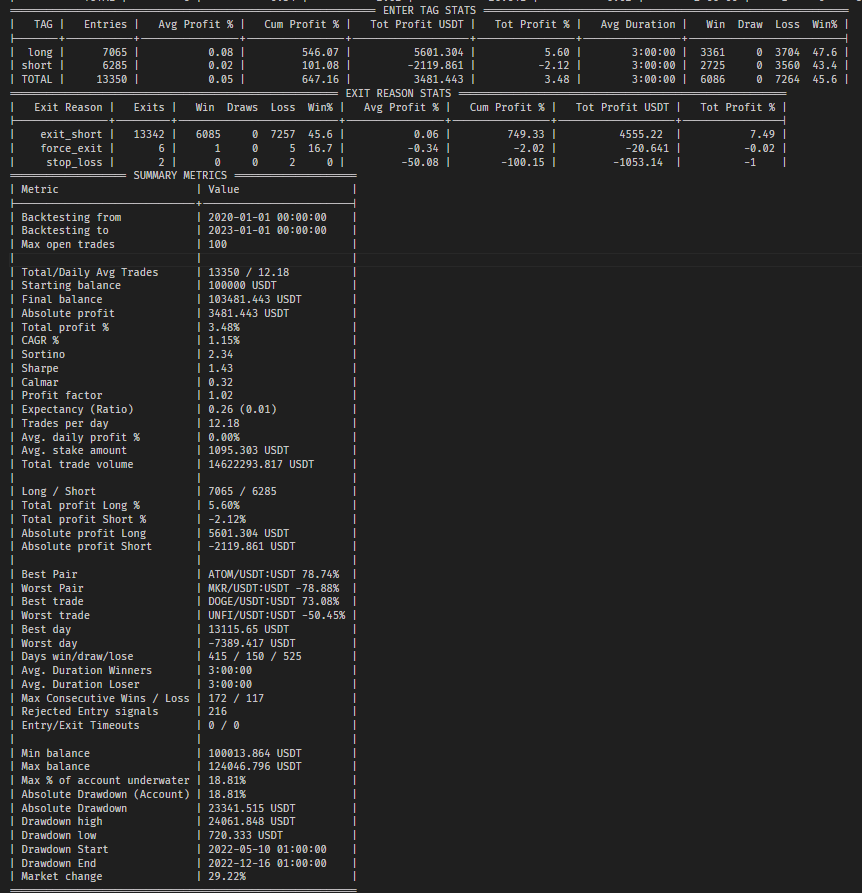

마지막으로 15시 매수매도, 레버리지 2배로 해보면

샤프는 매우 안정적인데, MDD가 30%인게 거슬린다. 게다가 9개월 동안이나 drawdown을 회복을 못하는게 좀 그렇달까

'투자 > 논문리뷰' 카테고리의 다른 글

| Impact of size and volume on cryptocurrency momentum and reversal (0) | 2023.12.29 |

|---|---|

| Momentum and liquidity in cryptocurrencies (0) | 2023.12.29 |

| Pure Momentum in Cryptocurrency Markets (0) | 2023.12.29 |